# load packages

library(tidyverse)

library(haven)

library(ggplot2)

# reading in the data

census_data <- read_dta("../datasets_beginner/01_census2016.dta")

# load self-tests

source("beginner_dispersion_and_dependence_tests.r")1.2 - Beginner - Dispersion and Dependence

econ 325

central tendency

descriptive statistics

variance

covariance

standard deviation

correlation

beginner

R

interquartile range

In this notebook we explore how data is spread out, and what that means for its interpretation. This includes both how individual values may vary, and how values may co-vary with one another.

Outline

Prerequisites

- Introduction to Jupyter

- Introduction to R

- Introduction to Visualization

- Central Tendency

- Distribution

Outcomes

This notebook explains the concepts of dispersion and dependence. After completing this notebook, you will be able to:

- Understand and interpret measures of dispersion, including variance and standard deviation

- Understand and interpret measures of dependence, including covariance and correlation

- Investigate, compute, and interpret common descriptive statistics

- Create summary tables for variables, including qualitative variables

- Parse summary statistics for meaning

References

Introduction

In this notebook, we will continue learning about how to use descriptive statistics to represent sets of data. We’ve already seen how to compute measures of central tendency and determine which measures are appropriate for given situations. We’ll now focus on computing measures of dispersion and dependence in order to better understand both the variation of variables, as well as relationships between variables in a data set. We’ll dedicate time to both measures, but we’ll look at dispersion first. Let’s first import our familiar 2016 Census data set from Statistics Canada.

Part 1: Measures of Dispersion for a Single Variable

Measures of dispersion describe the spread of data, that is, the possible values that a variable in a data set can take on. Common measures of dispersion which we’ll look at include the range, interquartile range, standard deviation and variance.

Range and interquartile range

The range of a variable is the difference between the maximum and minimum value that a variable takes on.

The interquartile range of a variable is the difference between the 75th and 25th percentile values of the variable. We can use functions like quantile() and fivenum() to calculate these statistics quite quickly.

Note: both

quantile()andfivenum()return the same output: a list with different percentiles of the data. By default, these are the minimum, 25th percentile, 50th percentile (median), 75th percentile, and maximum values.

Variance

The variance is the average of the squared differences from the mean.

- Small variance: observations tend to fall close to the mean

- High variance: observations are very spread out from the mean.

The formula for the sample variance is:

\[ s_{x}^2 = \frac{\sum_{i=1}^{n} (x_i - \overline{x})^2}{n - 1} \]

The formula for the variance in a population is:

\[ \sigma_{x}^2 = \int(x - \mu)^2 f(x) dx \]

Standard deviation

The standard deviation is the square root of the variance. It also measures dispersion around the mean, similar to the variance. For a sample this is:

\[ s_{x} = \sqrt{s_{x}^2} = \sqrt{\frac{\sum_{i = 1}^{n} (x_i - \overline{x})^2}{n - 1}} \]

For the population:

\[ \sigma_{x} = \sqrt{\sigma_{x}^2} \]

Example: a normal distribution with

mean = 30andsd = 5is exactly the same thing as a normal distribution withmean = 30andvariance = 25.

We usually use standard deviations rather than variances because the variance does not have the same units as the original variable, while the standard deviation does.

Advanced Note: In econometrics, some samples have more information than others about the population.For example, an estimate of the population variance based on a sample size of 100 certainly has more information than a sample size of 10. We measure the degree of uncertainty of an estimate using the degrees of freedom of an estimate. The degrees of freedom for our estimate of variance (sample variance) is equal to \(n - 1\).

In R, we use the var() function to calculate the variance of a variable, and the sd() function for the standard deviation.

# calculate the variance of wage

variance <- var(census_data$wages, na.rm = TRUE) # remember that we need to remove all NA valuesTest your knowledge

Calculate the standard deviation of wages by filling in the code on the cell below.

# fill in the ... with your code below to find the sd of wages - round your answer to the nearest whole number

answer_1 <- ...()

test_1()Interpreting Variation

Let’s say we’re interested in understanding how the wages variable is dispersed around the mean.

# recall the mean of wages

mean(census_data$wages, na.rm = TRUE)

# calculate the standard deviation of wages

sd(census_data$wages, na.rm = TRUE) We have a pretty large standard deviation - even larger than our mean! This tells us that most of the Canadians in the data set have a wage which lies approximately \(64275.27\) away from the mean of \(54482.52\).

This large standard deviation tells us that there is high variation in wages and that some of them are very far from the mean. This can be for many reasons, but one possibility is that we have outliers in the data set: extreme values of the variable wages. This is common for wage distributions in the presence of income inequality.

To Remember: the standard deviation is small when the data are all concentrated close to the mean, while the standard deviation is large when the data are spread out away from the mean.

Empirical Rule

Recall, from the Central Tendency notebook, that a very important distribution in econometrics is the normal distribution. For a variable with values distributed in this way, there is a quick way to estimate the density of the distribution with the standard deviation. This is called 68-95-99.7 rule or Empirical Rule:

- 68% of the values are within 1 standard deviation of the mean

- 95% are within 2 standard deviations of the mean

- 99.7% are within 3 standard deviations from the mean

- Remaining values are outliers and incredibly rare

This gives us a helpful frame of reference when discussing the standard deviation of a variable.

For example: let’s take test scores. Assuming test scores are normally distributed, if the mean score on a test is 70 and the standard deviation is 10, this tells us that approximately 68% of students who wrote that test earned a score between 60 and 80 (1 standard deviation), approximately 95% earned a score between 50 and 90 (2 standard deviations) and virtually everyone earned a score between 40 and 100 (3 standard deviations).

Test your knowledge

Let’s suppose the mean test score of my ECON 325 exam was 70 and the standard deviation was 5. If test scores are normally distributed and my grade was 85, what percentage of students got a grade higher than mine?

Hint: The area under the normal distribution has to sum to 1.

# write your answer in decimal form and don't round

answer_2 <- ...

test_2()Part 2: Measures of Dispersion for Multiple Variables

Measures of dependence calculate relationships between variables. The two most common are covariance and correlation.

Covariance

Covariance is a measure of the direction of a relationship between two variables.

- Positive covariance: two variables are positively related

- When one variable goes up, the other goes up, and vice versa.

- Negative covariance: two variables are negatively related.

- When one variable goes up, the other goes down, and vice versa.

This is similar to the idea of variance, but where variance measures how a single variable varies, covariance measures how two vary together. They also have similar formulas.

Sample Covariance:

\[ s_{x,y}=\frac{\sum_{i=1}^{n}(x_{i}-\bar{x})(y_{i}-\bar{y})}{n-1} \]

Population Covariance:

\[ \sigma_{x,y}=\int\int(x_{i}-\mu_x)(y_{i}-\mu_y)f(x,y)dxdy \]

This is tedious to calculate, especially for large samples. In R, we can use the cov() function to calculate the covariance between two variables. Let’s say we’re interested in exploring the covariance between the wages variable and mrkinc variable in the dataset.

# cov() function requires use="complete.obs" to remove NA entries

cov(census_data$wages, census_data$mrkinc, use="complete.obs") The calculated covariance between the wages variable and mrkinc variable in the dataset is positive, indicating the two variables are positively related. As one variable changes, the other variable will change in the same direction.

Let’s try computing the covariance “by hand” to understand how the formula really works. To simplify the process, we will construct a hypothetical data set with variables \(x\) and \(y\).

x <- c(6, 8, 10)

y <- c(25, 100, 125)# find the average values of x and y

avg_x <- mean(x)

avg_y <- mean(y)

# sum the products of the differences between the observations and the average

numerator <- {(x[1] - avg_x)*(y[1] - avg_y) + (x[2] - avg_x)*(y[2] - avg_y) + (x[3] - avg_x)*(y[3] - avg_y)}

# denominator is the sample size minus 1

denominator <- 3-1

print(numerator/denominator)# confirming the previous calculation

cov(x,y)Interpreting covariances directly is difficult because the size of the covariance depends on the scale of \(x\) and \(y\). Repeat the preceding calculation, but with variables that are 10x as large. What do you see?

x <- c(60, 80, 100)

y <- c(250, 1000, 1250)

cov(x,y)The solution to this problem is the next topic: correlation.

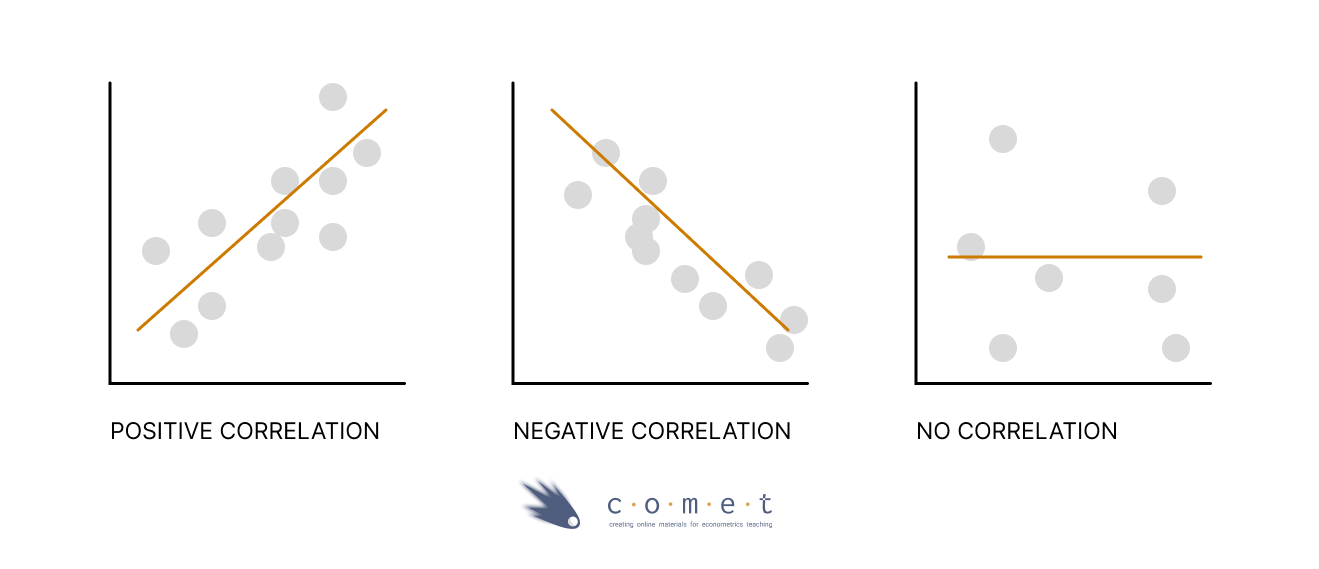

Correlation

A correlation coefficient measures the relationship between two variables. It allows us to know both if two variables move in the same direction (positive correlation), or in the opposite directions (negative correlation), or if they have no relationship (no correlation).

Note: even though a covariance or correlation may be zero, this does not mean that there is no relationship between the variables - this only means that there is no linear relationship.

Correlation fixes the scale problem with covariance by standardizing covariance to a scale of -1 to 1. It does this by dividing the covariance by the standard deviations of the variables. The most popular version is Pearson’s correlation coefficient which is calculated as follows.

\[ r_{x,y} = \frac{\sum_{i=1}^{n} (x_i - \overline{x})(y_i - \overline{y})}{\sqrt{\sum_{i=1}^{n} (x_i - \overline{x})^2 \sum_{i=1}^{n}(y_i - \overline{y})^2}}=\frac{s_{x,y}}{s_{x} s_{y}} \]

Once again, let’s try to compute the correlation “by hand” using the formula above.

numerator <- sum((x - mean(x))*(y - mean(y)))

denominator <- sqrt(sum((x - mean(x))^2) * sum((y - mean(y))^2))

numerator/denominatornumerator <- cov(x,y)

denominator <- sd(x) * sd(y)

numerator/denominatorIn R, we can use the cor() function to calculate the correlation between two variables.

# Confirming the previous calculation

cor(x,y)To calculate the correlation between the wages variable and mrkinc variable in the dataset:

# cor() function requires use="complete.obs" to remove NA entries

cor(census_data$wages, census_data$mrkinc, use="complete.obs") Now we have the number 0.8898687 \(\approx\) 0.89 as our correlation coefficient. What does it really mean?

A correlation coefficient ranges from -1 to 1, which tells us two things:

The direction of the relationship between the 2 variables.

- A negative correlation coefficient means that two variables move in opposite directions. If a variable increases the other decreases and vice versa.

- A positive correlation implies that the two variables move in the same direction, that is, if one variable increases the other also increases and vice versa.

The strength of the relationship between the 2 variables.

- The more extreme the correlation coefficient (the closer to -1 or 1), the stronger the relationship. The less extreme the correlation coefficient (the closer to 0), the weaker the relationship.

- Two variables are uncorrelated if the correlation coefficient is close to 0. As one variable increases, there is no tendency in the other variable to either decrease or increase.

We can also easily visualize the correlation between two variables by plotting a scatter plot with a trend line via the ggplot() function.

# scatterplot of market income against wages

ggplot(census_data, aes(x = mrkinc, y = wages)) +

geom_point(shape = 1)Adding a trend line to the scatter plot helps us interpret the directionality of two variables. We can do it via the geom_smooth() function by including the method = lm argument, which displays scatterplot patterns in the presence of overplotting. You will learn more about how trend lines are mathematically formulated in advanced econometrics classes.

ggplot(census_data, aes(x = mrkinc, y = wages)) +

geom_point(shape = 1) +

geom_smooth(method = lm) # add this argument to draw the trendlineNow we can see the apparent positive correlation!

Test your knowledge

Is the following statement True or False?

The correlation coefficient adjusts the measure of covariance so that it can measure linear relationships.

answer_3 <- "..." # enter "True" or "False"

test_3()Suppose the weights of packages(in lbs) at a particular post office are recorded as below.

package_data <- c(95, 130, 148, 183, 100, 98, 137, 110, 188, 166)# calculate the mean, standard deviation and variance of the weights of packages

# round all answers to 2 decimal places

answer_4 <- # enter your answer here for mean

answer_5 <- # enter your answer here for standard deviation

answer_6 <- # enter your answer here for variance

test_4()

test_5()

test_6()Use the example above to answer: Assuming the weights follow a normal distribution, 68% of packages at the post office weigh how much?

- 68% of packages weigh between 65.30 and 150.70 lbs

- 68% of packages weigh between 100.40 and 170.60 lbs

- 68% of packages weigh between 120.40 and 150.60 lbs

- 68% of packages weigh between 80.56 and 120.60 lbs

answer_7 <- "..." # enter your choice here (ex, "F")

test_7()Now, brainstorm some real-world examples that best demonstrate the correlation relationships below. The first one is already done for you!

- zero or near zero: the number of forks in your house vs the average rainfall where you live

- weak negative:

- strong positive:

- weak positive:

- strong negative: